5 Biggest Mistakes When Buying a Home in Silicon Valley

Tips in Buying or Selling a Home

Tips in Buying or Selling a Home

Buying a home in Silicon Valley can be a daunting proposition. Not just because the prices are so high (as of April 2023, the median price of a single family home is $1.8M), but also because there are so many other serious home buyers all vying to buy the same home you want to buy! Knowledge is power, as they say, and buying a home in the epicenter of “tech” means leveraging not just the latest apps to alert you about the housing market or the latest home for sale, but also getting the right advice about what to do and not to do.

The housing market is ever changing, whether from economic influences or from new laws that impact our real estate practices. So no matter how experienced or inexperienced you may be in home buying, when you’re competing with other very serious home buyers for a home in Silicon Valley, there’s a bit of a mind-set shift that’s required if you truly want to have your offer accepted. These 5 topics are undoubtedly the most common mistakes that we try to course-correct and educate clients on before they put in an offer!

For buyers that don’t absolutely need to buy a home, this is one of the most common mistakes I see. Silicon Valley is filled with very savvy people that are used to relying on data analytics, economists, and in-house experts to successfully run their businesses. So when they decide they’d like to buy a home that better fits their ideal lifestyle and dream, they apply the same thoughtful analysis and approach. That works well until new data is published somewhere that suggests there could be changes in the economy that could impact housing. That’s when the brakes get applied and the concern about making a poor financial decision overrides all else.

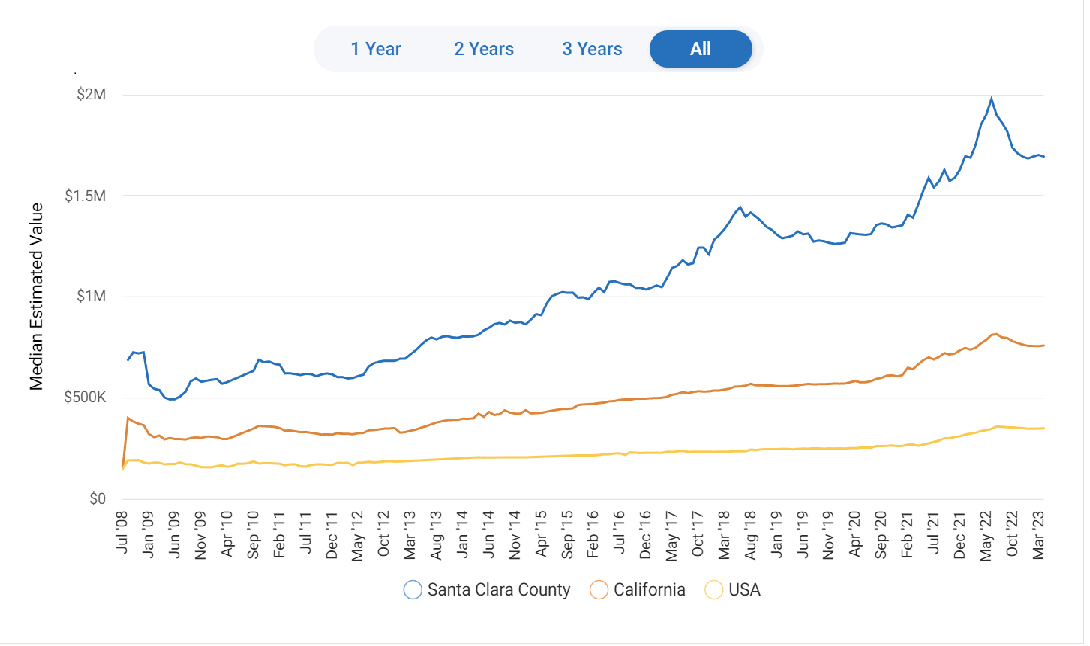

Of course no one wants to make a bad financial investment! When clients get worried about economic forecasts showing housing prices going up or headed down, it’s important to remember that homes in Silicon Valley have generally doubled in price every 10 years. Yes, there have been dips in price and we’re currently rising out of the dip that started in mid-2022, but over time, the market bounces back and then continues on its ascent.

Single Family Home - Median Prices Over Time Source: Realtors Property Resource, LLC

Don’t Wait if You Plan to Stay: If you plan to be in your home for 5 or 10 years, then timing the market for when there’s less competition or lower interest rates or more favorable market trends is a mistake as there’s never a perfect time. I’ve seen way too many situations of clients kicking themselves that they didn’t act as aggressive as we knew they needed to, simply because of their fears about the market. They decided to wait for prices to stabilize or come down, or interest rates to come down, or some other economic reason, only to find themselves staying on the sidelines for so long that now they no longer qualify for a home anywhere near the size and style they could have purchased 2 years ago.

A different lens from which to look at buying a home is that this is more than a financial investment, it’s one that you get to use, to live in, and to enjoy. We all have to live somewhere, and this is an investment that provides a sense of stability and financial security, and allows you to build equity and wealth, and create a sense of community. If a home purchase is for the long term, then what the market does day-to-day is less relevant in the long run. The point is that if this is a home for you and your family to live in, then over time, whatever market blip occurs is only an issue if you are selling your home at that moment.

This is a more common mistake with first time home buyers, but it also serves as a good reminder even for home buyers that are seasoned homeowners. I’ve seen many would-be homebuyers jump in quickly to want to put in an offer on a home, only to pull back abruptly once they learn that the costs to upkeep the pool, landscaping, etc of the home is just beyond their budget.

Buying a home is a significant financial decision that involves more than just the purchase price. It’s very common to focus on the upfront costs like the down payment, as that’s usually the biggest hurdle to buying a home. But it's essential to consider the other expenses associated with the process. These costs can add up quickly and impact your overall budget. Here are some of the other costs to consider:

Closing Costs: The fees and expenses associated with finalizing the home purchase are known as the closing costs. These costs typically include appraisal fees, title insurance, escrow fees, loan origination fees, home inspection fees, and various other administrative charges. Closing costs can range from 1% to 3% of the home's purchase price, so it's important to budget accordingly.

Lender Requirements for Reserves: Lenders may require borrowers to have a certain amount of money set aside as reserves. These reserves act as a safety net to ensure homeowners can make mortgage payments even in the face of unexpected financial challenges. Lenders usually require a certain number of months' worth of mortgage payments to be held in reserve, which can vary depending on the lender and loan type.

Property Taxes: Property taxes are an ongoing expense that are paid twice yearly, or they can be added to your monthly mortgage bill. The amount you pay in property taxes depends on the assessed value of the home and the tax rates for your county and city services. Because of California’s Prop 13, which was passed back in 1978, the maximum your property tax will will increase each year is 2%. So seeing what the current owner pays for property taxes can be misleading if they’ve lived there for many years. A good rule of thumb to figure out your potential tax rate is to multiply the purchase price of the home times 1.25%.

Homeowners Association (HOA) Fees: If you're buying a property within a planned community or a condominium, there may be HOA fees to consider. These fees cover maintenance and shared amenities within the community, such as landscaping, pool upkeep, security, and common area maintenance. HOA fees vary widely depending on the community and can range from modest to substantial, impacting your monthly housing costs.

Home Insurance: Mortgage lenders will require you to secure a homeowners policy prior to closing escrow to protect against potential damages or loss to the property. Home insurance premiums can vary based on factors like the location, size, and value of the home, as well as the coverage options you choose. It's crucial to obtain insurance quotes and factor in the ongoing cost of insurance when budgeting for your new home.

Utilities, Maintenance and Repairs: If you’ve been a homeowner before, you know to plan for these. But if this is your first home or you’re buying a larger home or one with higher upkeep due to a pool or land, it’s helpful to understand what the current homeowners are paying for some of the ongoing utility expenses and maintenance costs like landscaping, pest control, and cleaning. Setting aside funds for unforeseen repairs such as plumbing issues, roof leaks, or appliance breakdowns is essential to ensure you can handle them when they arise.

Let’s face it, no one wants to overpay for anything, not for a meal, not a car, and definitely not for a home. It's a source of pride to have bragging rights about the amazing “deal” you just landed.

So it’s not surprising that, when faced with feedback from the seller that the offer price you just submitted isn’t in the running to “win”, the immediate reaction is one of surprise followed by caution. If we go to a higher price, will the bank agree that it’s worth the new value? Is the home worth a higher price? Can I afford a higher price? Add to it, it’s usually with the added stresser that the listing agent needs an answer with your new offer in writing in the next 30 minutes!

This is where all your analysis from Zillow or Redfin and data from recent home sale prices can trip you up. Keep in mind that the Internet has never been inside this home, and doesn’t know it’s fabulous floor plan or excellent lighting. Plus in a market where prices are trending up, your offer may indeed be higher than comparable properties because a new baseline is being established. When you’re in the middle of rising market it can feel like you’re overpaying.

In time, you'll look like the smartest person ever to have purchased a home in that area at such a great price. It’s all relative!

Here’s what I mean, let’s say you fall in love with the perfect home and all the market data supports an offer of $1.2M, but then you find out you’re one of 10 offers and there are several of you that are all matched in terms and price. If no other term can be adjusted to appeal to the sellers, then that’s when price is the only way to stand out. The past data says $1.2M max, but whoever buys this property will pay more than that to “win”. If going a bit over your offer price is the way to “win”, it’s best to consider all the factors, including whether that price increase is do-able with your monthly budget. If you decide to increase your offer or decline, whomever purchases the home, the price that's paid to the sellers will contribute to setting the new price point and baseline for homes in the area.

This is where your realtor needs to understand the approach the listing agent is taking for reviewing offers. There is no rule of thumb or standard practice when it comes to buying residential real estate. Each transaction is unique. Sellers may have a circumstance that’s driving their decision process, and the real estate agent may have a tried and true approach to how they respond to offers. That’s why it’s pivotal to understand, as much as you can, how this sale is expected to be handled.

If the listing agent and sellers are willing to negotiate and counter the buyers’ offers, this is the best and most fair circumstance. If your offer is in the top tier of offers, then you will typically be given a chance to resubmit your offer or the seller will send you a counter offer, and from there you can decide your next steps. Putting in too low of an offer means you don’t get this opportunity, which is why it’s never advised to put in an offer and expect to negotiate. This isn’t commercial real estate or a car purchase.

The only rule is that the listing agent has to share your offer with the seller. The seller has no obligation to respond to your offer.

The circumstance that’s the most difficult in determining an offer price is when the listing agent says to put in your “best and final” offer. This usually means the seller is planning to just sign the best offer and has no interest in doing any sort of counter offer. If you’re competing with other buyers, it’s now like playing poker. None of the other buyers knows what the other is offering, and most listing agents won’t share. This is where you need an experienced agent to help you navigate and look at all the options, all the current and past sales, the amount of competition, and in the end, go with your gut. I know that sounds odd, but there are times where decisions go beyond the data.

If the home feels right and it’s the place where you can really see yourself making new memories with your loved ones, then sometimes you just gotta jump in and go for it!

If you're planning to buy a home with a loan, it’s important to use a lender (typically a local one) that understands the Silicon Valley market and has a strong track record of success. Many buyers have taken the first step on their own, and researched lenders to find the best rate, or have contacted an online lender or the mortgage lender at their local bank, or even spoken with a lender that was referred by a friend. Sometimes this works out, but the mistake is not understanding that not all lenders are well experienced in Silicon Valley real estate purchase loans. Unless the lender is accustomed to our local practices and accelerated terms, the loan terms they offer may not be acceptable to a seller nor competitive enough for you to “win” in a multiple offer bidding war.

All Cash, Non Contingent Offers: Silicon Valley is a market where home buyers are known to put in offers of all-cash with “no contingencies”. These all-cash buyers will have a leg up on buyers that need a loan because they can often close escrow very quickly (as little as a few days) and don’t need to include any loan or appraisal contingencies in their offer. That means there isn’t another party (like a lender) that could force the buyer to back out of the transaction (i.e. if their loan isn’t approved). An all-cash offer is the lowest risk offer to a seller and the one most enticing for a seller to accept.

Pre Approval and Underwritten: So to level the playing field, buyers in Silicon Valley work with lenders that will pre approve and underwrite them. This means the lender does the exhaustive due diligence work up front to confirm all their financials prior to finding a property to buy. This type of pre approval with underwriting positions buyers to also make offers that have no loan or appraisal contingency with very swift escrow closings. The key is that this is done with very careful planning and risk analysis. Buyers that opt to remove their contingencies need to have a very high degree of confidence that their loan will be approved (and sellers want to see that too). Otherwise, buyers risk losing their deposit if they have to back out of a transaction without a contingency to do so.

Another benefit of having a lender underwrite a buyer before they go into contract on a home purchase, is that the lender has now already completed many of the loan approval steps and can reduce the number of days necessary to close escrow. In our area, it’s quite standard to see a 21 day close of escrow and even as little as 12 days. Nationally, close of escrow periods are typically 30-45 days.

Direct Access: The other, less data-driven aspect but of high import is having a highly accessible lender that can be reached directly. Having a lender that is willing to reach out to the seller’s agent and share the strength of your offer demonstrates that the lender knows you and has spent time delving into the financial viability of you purchasing the home. When all the offers look similar, having a lender that’s hands-on and takes the time to underscore the financial strength of a buyer can go a long way in giving the seller confidence that the lender is committed to closing escrow. This type of direct access to a lender throughout the escrow process can be pivotal in both winning the bid and closing escrow on time.

Sometimes it takes more than one offer to get your offer accepted, even when you know all the potential pitfalls! It's important to take your time and do your research. And when you’re ready, just like any other major decision in your life, having an A-team of advisors advocating for you and guiding you will give you the highest chances of successfully purchasing your dream home! Happy house hunting and please reach out if you’d like to start the conversation about buying your next home in Silicon Valley.

Hello! I'm Janet Souza, lifestyle blogger and REALTOR® at Christie's International Real Estate Sereno. I live and work in Silicon Valley and love everything our wonderful area has to offer. If you live in Silicon Valley or are thinking about moving here, you've come to the right place! Stay up to date with local events, theater, concerts, Real Estate and more!

Cookies

The Perfect Lemon Crinkle Cookies to Brighten Any Open House or Spring Gathering

News In The Community

A curated guide to music, culture, and spring experiences happening around Silicon Valley this month.

Fundamental to how Janet Souza views her role as her client’s real estate advisor, she seamlessly blends her former professional worlds that span consulting, engineering, marketing, strategy, and executive sales negotiations as her frame of reference, bringing a premier standard of performance and uncompromised integrity to her clients.